Apple's share opened around 113 USD today. Right now, however it has climbed to 115 USD. When I last looked at the stock and wrote a few lines here (previously also here and here) it was at 109 USD, and I thought it was more or less fairly priced. I still think so, but perhaps slightly on the expensive side, considering how competition is heating up in phones, tablets and watches.

Reviewing ML's update on Apple

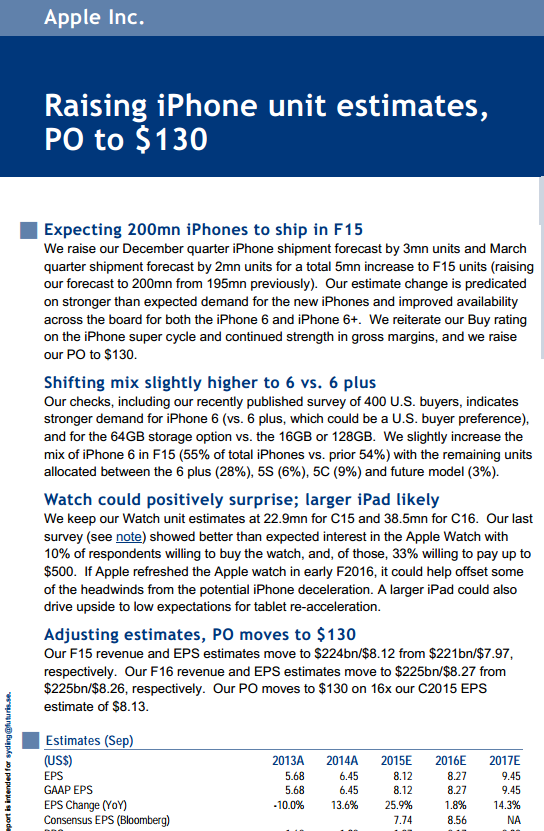

Earlier in the day, Bank of America Merrill Lynch released a new research report on the company (just 15 pages). In it Merrill's analyst upgraded his price objective to 130 USD per share from 120, based mainly on his increased estimate for iPhone unit sales estimate in Fiscal Year 2015 from 195 million to 200 million, i.e., by 2.5%.

The forecast for the following year, 2016, is lower; just 187m units, whereas my Quick and Dirty forecast for 2016 is 201m units so nobody can accuse me of being pessimistic...)

EPS estimate raised by 0.1%, price target by over 8%

The FY 2016 EPS estimate is raised by one full cent from 8.26 to 8.27. Since the analyst bases his price objective on forward P/E, he has thus suddenly increased his main valuation objective by almost 10 per cent from 14.5 to 15.7. Why? No reason is put forward for why the more representative year of 2016 is ignored and the "iPhone 6-year" of 2015 is chosen instead.

He (of course) has a Buy rating, which is perfectly OK with a price objective 13-15% higher than the current trading price. However, it is still a bit optimistic considering the average forecast among other analysts is an EPS of 8.56 for 2016 compared to BofA's 8.27.

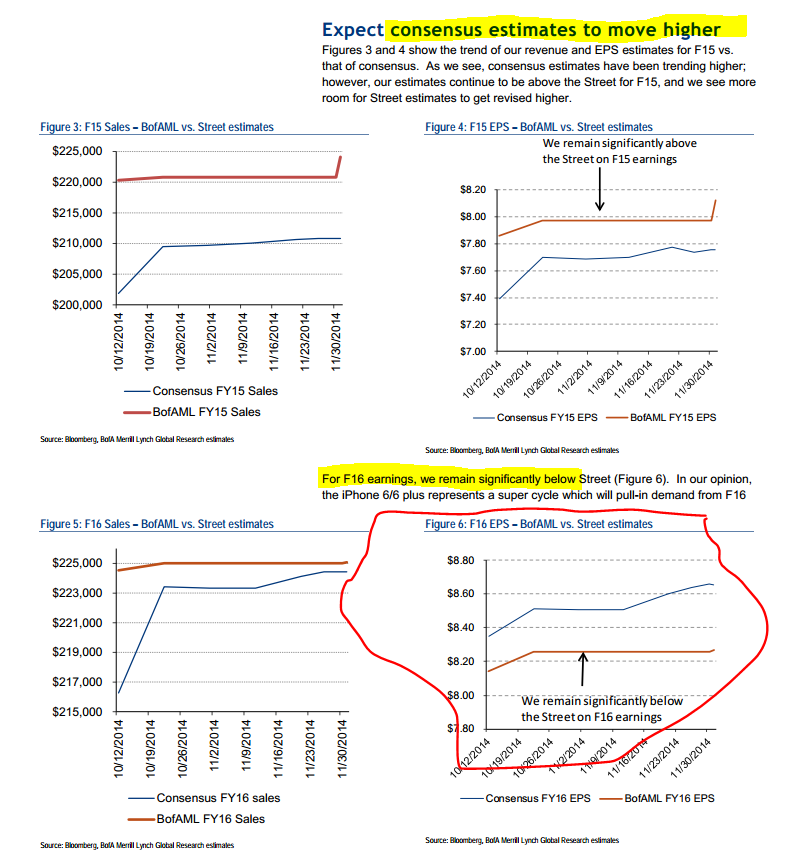

This headline is quite misleading, telling the reader that estimates will rise... but that's for 2015. They try to hide the situation in 2016 where consensus estimates need to fall to approach BofA's estimate:

1. No explanation for why the key metric (iPhones) is increased by 2.5% and EPS next year only by 0.1% (the reason is that the iPhone 6 is expected to only have short term effects and thus shouldn't affect EPS, valuation or target price)

2. No explanation for why the valuation target is increased by more than 8%, i.e, the target price is increased by 8.3% despite basically no change to the earnings forecast

3. Misleading headline on likely forecast changes (the ones that matter)

Complicated and unnecessary tables for no reason

The sell side loves making tables like this one; it looks serious but it adds nothing in terms of understanding the company or its valuation:

4. Trying to build credibility via unnecessary charts

Using wholly unrepresentative year as base for valuation of 50 years' cash flow stream

It's bad enough, albeit pragmatic in today's environment, to base price objectives and recommendations on P/E ratios. What's worse is that the target price is based on the 12 month forward (Calendar 2015) EPS which is extremely heavily affected by the launch of the iPhone 6. In addition the reader only gets to see forecasts up until FY 2016 and is supposed to for an investment strategy on 2 years of forecasts in a market with a duration of 50 years:

5. Deceptively detailed forecasts on geography, phone models, business areas etc:

6. Forecasts only range to 2016

History of price targets tell a familiar story of permabullishness and lack of independence

The following chart is a great laugh; the Price Objective is constantly changed to make sure there is always a 15-20% upside in the stock price.

7. It's good they are forced to present that final chart. It's bad they don't analyze it and explain it to the reader.

Please note that I have no quarrel with ML or its analyst. Rather I think BofAML is among the better research houses, not least their IT and technology analysts. Also note that I don't really disagree with the forecasts or the conclusion - although my QaD analysis has a lower target price. Apple is an interesting case, since it is so big, so well researched and is trading close to fair value given what we know today (albeit not given the risk of black swans, recessions, competition or rising interest rates).