Not as in it was easy, but as in it was naïve, crude, unreliable, playful.

The Amazon case just a crude beginnng, or even just the start of a beginning. There are so many other variables to check and analyse before you can trust your model the least bit:

Are the numbers correct and comparable? Don't take accounts at face value. No not "even" audited numbers from publicly filed reports. There are acquisitions and accounting rules, revenue recognition issues etc. that changes or obscures the real underlying fundamental trends.

Forecasts ar not supposed to be just extrapolations. They should be based on the actual business and business environment of the company in question. That means you must understand the business to make forecasts, just as you had to understand the horse and carriage businees when the car arrived or the typewriter business when the computer struck the market.

Business cycles. Amazon won't grow forever. And even if they did, your valuation should account for cyclical ups and downs, as well as mistakes and inventions. It doesn't have to be rocket science level calculations, but make sure you are explicit and thorough and annotate your model meticulously.

A shorthand is allowed of course, e.g. an average growth rate or average steady state margin. Just remember that is all it is, in reality there will be peaks and troughs in sales and margins. Regarding the shares there will be other peaks and troughs in the valuation of the cyclical earnings - often high valuation of high profits and low valuation of low profits, even though the opposite would be more correct. That's what creates opportunities.

You want to buy when people are in a state of panic, when both profits are low and the valuation of those profits are low.

Total available market; how long can they grow? What substitutes and competitors are there. How are clients' tastes changing, as well as their ability to pay?

Forecasting Walmart

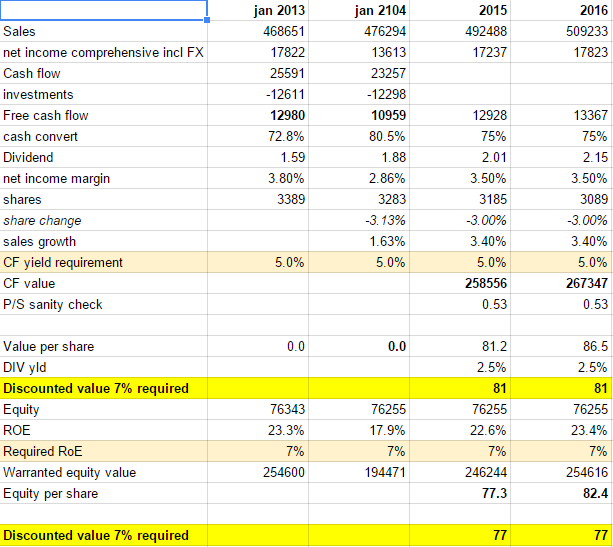

Walmart's net sales have grown by 0.9%, 3.4%, 6.0%, 5.0% and 1.6% respectively the last 5 years. The average and the median are both 3.4% so let's use that as our forecast going forward. However, nota bene, sales growth per store that has been open for the entire year has been much lower. Quirks like that can matter but disregard that for now.

Gross margins have fallen slightly year by year over the five year period, from 24.9% to 24.3%. On the other hand Operating costs (also called "opex" for Operating Expenditures) have also fallen as a percentage of sales. Anyway, operating income has increased by about 3.0% per year during the period, but stock buybacks (at a rate of 7bn USD/year the last three years) and possibly lower taxes have contributed to a faster rise in EPS (earnings per share):

EPS: 3.72, 4.18, 4.53, 5.01, 4.85 (total growth 30%, average annual growth in EPS 6.9%)

Net income the last three years have been 15.7bn, 17.0bn and 16.0bn respectively. However, including FX losses N.I. dropped significantly in fiscal 2014 (January): 2012: 13.6bn, 2013: 17.8bn, 2014: 13.6bn. So, make sure you pay attention to movements in currency exchange rates ("FX" or "F/X") and their effects - not least when making forecasts.

Also note that Walmart's assets have increased by 20% since 2010 and its equity by 8%. These numbers aren't that important in this case, but they could have been. You want to check if the company ties up more and more assets or if it's becoming leaner (or too lean). Check all items in the balance sheet and if anything changes by much from year to year, either nominally or as a proportion of total assets or net sales or in relation to other items in the balance sheet, dig deeper. In particular you want to check for balance sheet items called "other", just as you want to check P&L items called extraordinary or one-off.

Days of sales outstanding (DSO) is particularly important for companies selling big ticket items (like Oracle, e.g.). Their invoices typically get paid within 60-90 days or so. If that number increases it means the company is overselling, invoice stuffing its clients, or is having trouble getting paid by its clients (bankrupt?). Hence, check carefully for increases in receivables/sales and decreases in payables/sales.

Then it's time to check cash conversion rates (from net income to actual free cash flow) and the company's cash usage and cash balance. Walmar's cash at hand, e.g., dropped by 0.5bn to 7.3bn in fiscal 2014, despite making 11bn in cash flow before financiing activities. Changes in debt, stock repurchases (6.7bn) and stock dividends (6.1bn) explain the difference. Nothing strange here, but you always need to check there aren't any funnies or numbers that don't add up.

As far as a quick and dirty valuation goes, you are about done with the history at this point. However, as a serious investor you really should go through all footnotes, read and re-read the previous five annual reports looking for discrepancies and changes in numbers and accounting practices like revenue recognition rules, net working capital, tax rates, acquisitions etc. Every number should be turned upside down and inside out before you are ready. You should read about and understand its competitors, suppliers and clients as well. In the best of worlds you should build models for them too (if they are big and the data is available).

We won't do that now. Walmart is a fairly easy case anyway; they sell a million different quite cheap goods and they grow in line with world nominal GDP. There sholdn't be any big surprises there. Further, its cash conversion from net income after taxes and FX effects is not further from 100% than our safety margin in valuation must be in any case. CC in 2013 and 2014 was 72.8% and 80.5% respectively.

If you count on dividends along the way don't forget to take them into account (plus for you as a shareholder but minus in the accounts as a cash outflow. Share buybacks work by reducing the number of shares in the EPS calculation and is also a cash outflow for the company)

Why Walmart's shares might just be a good Buy

This really QaD model of Walmart, that I just put together says its stock should be worth 77-81 USD (it's trading at 75.85 right now. Given my assumptions it's a reasonable buy):

The really key assumptions here are the valuation parameters. I have assumed Walmart's business model warrants a required return on equity of 7% per year, or in free cash flow terms, a 5% annual CF yield. The P/S sanity check renders a valuation of 0.5x sales for a company growing in line with the economy and a net margin of 3.5%. Sure, I can take that. It's not cheap, but it's reasonable - not least in this environment.

Summary

Pay attention to details if you are going to do this for real. Net working capital, DSOs, stock option renumeration accounting, revenue recognition rules, tax rates, FX effects, business area particulars, competitors, commodity prices, business cycles, debt situation, lease contracts, valuation methods (DCF, P/E, P/S, EV/S, yields), short interest, buyback programs... There are hundreds of more or less quirky variables that hundreds of thousands of analysts get paid hundreds of thousands of dollars, if not several million, per year to keep up with.

These last two posts don't even come close to being real models or real research on either company. A typical model runs hundreds, if not thousands, of lines long, not to mention hundreds of columns wide, with decades of quarterly and monthly data - sometimes even daily or weekly data on frequent data like weather.

More is not necessarily better, but you need to know a lot of things before throwing your money on something that just might be the next Enron.

However, I still think you can do it if you want to

Work smarter, not harder, than the drones at the large investment banks.

A final question - comparing Walmart and Amazon

If more or less the same approach says Walmart is reasonably valued and Amazon is 10x overvalued; How come people buy Amazon's stock?

What do you say? Do you own any of these?

Do you want to keep getting my opinion on things like Amazon and Walmart? SUBSCRIBE (upper right of the page). YES, please.